Creating a budget is one of the easiest ways to take control of your money and stop worrying about overspending. A budget helps you track your income, manage your expenses, and save consistently so you always know exactly where your money is going.

In this guide, you’ll learn how to create a budget step-by-step. You’ll discover simple, practical ways to plan and adjust your finances to fit your lifestyle.

By following these steps, you can build a budget that works for you, keeps your finances on track, and helps you reach your money goals every month.

Ready to transform your financial life? Let’s get started!

Why Creating a Budget Is Important

Before diving into the steps for creating a budget, it is essential to understand why it is important to have a budget.

Many people hear the word “budget” and think it means restriction. But that’s not what budgeting is really about. Budgeting is about clarity and control. Without a clear plan, it’s easy to overspend, put off your savings goals, and feel stressed about money.

A budget gives you a clear view of your spending and shows exactly where your money goes each month. This visibility helps you make smarter financial decisions, avoid unnecessary expenses, and prioritize what truly matters to you.

Here’s why creating a budget can make a real difference:

- Shows where every dollar goes. Tracking expenses, including small daily purchases, helps identify areas to adjust and improve.

- Encourages consistent saving. A budget makes it easier to set aside money for emergencies, long-term goals, or big purchases.

- Prevents overspending. Assigning limits for each spending category keeps you in control and avoids month-end surprises.

- Reduces financial stress. Knowing your money is accounted for gives peace of mind and allows you to plan ahead confidently.

Pro Tip: Think of a budget as a guide that gives you clarity and control. It’s not meant to restrict you but to help you make intentional choices with your money.

“A budget is telling your money where to go instead of wondering where it went.” – Dave Ramsey

How to Create a Budget: 6 Simple Steps

Creating a budget might feel overwhelming at first, but breaking it into simple steps makes it much easier. Follow these steps to build a budget that helps you track your money, set limits, and take control of your finances.

Step 1: Calculate Your Real Income

Before you do anything else, you need to know how much money you actually have available each month. This means focusing on your take-home pay after taxes and deductions, not the salary you see on your offer letter.

A quick way to calculate this:

- Check your last two or three paychecks.

- Add them together.

- Divide by the number of pay periods to get your actual monthly income.

If you’re self-employed or your income varies, use the lowest monthly average from the past six to twelve months. While this might feel conservative, it gives you stability during slower months and keeps your budget from falling apart when income dips.

Once you have this number, everything else becomes much easier to manage.

Step 2: Track Your Current Spending

This step makes most people uncomfortable, but it’s also the most eye-opening. You can’t build an effective budget without understanding where your money currently goes.

You can track your spending in two ways:

Option A: Review Past Transactions

Look at your bank statements, debit or credit card history, receipts, and any automatic subscriptions. This gives you a quick snapshot of your spending habits.

Option B: Track Forward for 30 Days

To understand your current habits, start by tracking every single expense for a full month. You can use a notebook, a spreadsheet, or a dedicated expense tracking app. Don’t skip small purchases, as they add up quickly.

Organize your expenses into categories, such as:

- Income: all money coming in.

- Food: groceries, dining out, snacks.

- Transport: gas, rideshares, public transit.

- Rent / Housing: rent, utilities, maintenance.

- Shopping: clothes, gadgets, online orders.

- Miscellaneous: anything that doesn’t fit elsewhere.

Once you record everything, review your spending patterns. You might notice unexpected trends, like frequent takeaway meals, recurring subscriptions, or impulse buys. Recognizing these patterns is crucial because it helps you make informed decisions, set realistic limits, and adjust your spending to match your lifestyle.

Tracking your monthly expenses helps you understand your spending patterns, making it easier to manage your money and reach your financial goals.

Step 3: Organize Your Expenses Into Categories

Now that you know where your money goes, it’s time to group similar expenses into budget categories. This creates structure and makes it much easier to control your spending.

Here are beginner-friendly categories that work well:

- Housing

- Bills and Utilities

- Groceries

- Transport

- Insurance

- Debt Payments

- Savings

- Entertainment

- Shopping

- Miscellaneous

Your categories don’t need to be perfect. Keep them simple and adjust them later as you get more comfortable with budgeting. The goal is clarity, not perfection.

Step 4: Set Clear and Realistic Spending Limits

Now your budget becomes a real plan. You know your income and spending patterns, so it’s time to assign limits to each category.

Start with fixed expenses you cannot change easily:

- Rent or mortgage

- Utilities

- Insurance

- Debt payments

After that, move to flexible categories:

- Groceries

- Transport

- Entertainment

- Dining out

- Shopping

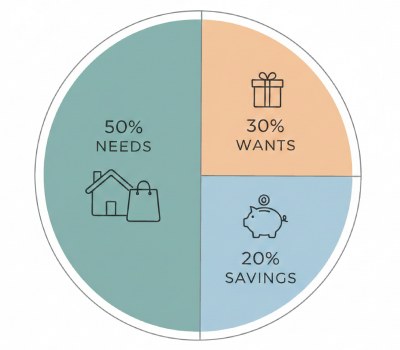

If you want a helpful guideline, the 50/30/20 rule is a great starting point:

- 50% for needs

- 30% for wants

- 20% for savings or debt repayment

Some people prefer zero-based budgeting instead, where every dollar gets assigned a specific purpose. This helps keep your budget balanced and prevents overspending in any one area.

If you want to skip the math, try our budget calculator. It automatically applies the 50/30/20 rule and shows you how much you should ideally spend in each category based on your income.

Be honest when setting your limits. Many people underestimate groceries or assume they’ll drastically cut entertainment spending right away. Set limits that match your real life. You can tighten them later once you build a consistent pattern.

Pro Tip: You can use a budget planner that allows you to create a budget by categories, record your transactions, and send you alerts when you are close to your budget limit. This makes it much easier to stay on track and avoid overspending.

Want free tools? Check out our free budget apps Guide for the best apps to help you manage your money without spending a dime!

Step 5: Adjust and Rebalance Your Budget

Your first budget won’t be perfect, and that’s completely normal. Budgeting is a skill that improves as you practice and adjust it over time.

Review and rebalance your budget when:

- Your income changes

- Your expenses increase or decrease

- You consistently overspend in a specific category

- Your priorities or lifestyle shift

Think of your budget as something flexible that grows with you. It’s not meant to stay the same forever.

Step 6: Review Weekly and Revise Monthly

Weekly check-ins are the secret to staying on track. They only take a few minutes and help you stay aware of your spending.

Each week, ask yourself:

- Which categories are close to their limits?

- Which categories still have room?

- Do I need to slow down my spending?

At the end of the month, take time to reflect:

- What went well?

- Which limits were unrealistic?

- What needs to change for next month?

These small, consistent reviews turn budgeting into a habit instead of something you try for one month and then abandon.

Conclusion

Learning how to create a budget is one of the most valuable things you can do for your financial stability and peace of mind. It helps you understand your habits, make smarter decisions, and stay in control of your money instead of feeling overwhelmed by it.

Your first budget might feel messy, but it gets easier every time you revise it. Eventually, you’ll start noticing spending patterns, cutting unnecessary expenses, and saving more for the things that matter most to you.

Budgeting isn’t about restriction. It’s about creating a plan that supports the life you want. And the best part? You can start right now with these simple steps. A month from today, you’ll be glad you did.

FAQs

Q1. How many categories should I include in my budget?

Start with 8 to 10 simple categories like housing, groceries, transport, bills, savings, and entertainment. Once you get comfortable, you can refine or add more categories based on your lifestyle.

Q2. Which budgeting method is best for beginners?

Most beginners find the 50/30/20 rule or a basic category-based budget easy to manage. Choose the method that feels natural and helps you stay consistent over time.

Q3. What if my budget doesn’t work the first time?

It’s completely normal for your first budget to need adjustments. Keep tweaking your categories and spending limits until they reflect your real financial habits.

Q4. Can I budget if my income changes month to month?

Yes, you can budget with irregular income by using your lowest reliable monthly income as the base. Any extra income can then be used for savings, debt, or financial goals.

Q5. How long does it take to see results from budgeting?

Most people begin noticing positive changes within one to two months as spending becomes more mindful. With consistency, the progress becomes faster and more impactful.