Imagine you’re building a new house. You wouldn’t just look at your old house and decide to add a few more windows and rooms. Instead, you’d start with a blank blueprint, carefully designing every single room and feature from scratch. 🏡

This is exactly how zero-based budgeting (ZBB) works. It’s a method that gives every single dollar a purpose, helping you stay intentional with your money. Before we dive deeper, it can help to first understand what is budgeting, which provides the foundation for managing your money effectively.

Let’s break down zero-based budgeting in simple terms so you can see exactly how it works.

What is Zero-Based Budgeting?

Zero-Based Budgeting is a budgeting method where every expense must be justified from scratch at the start of each financial period.

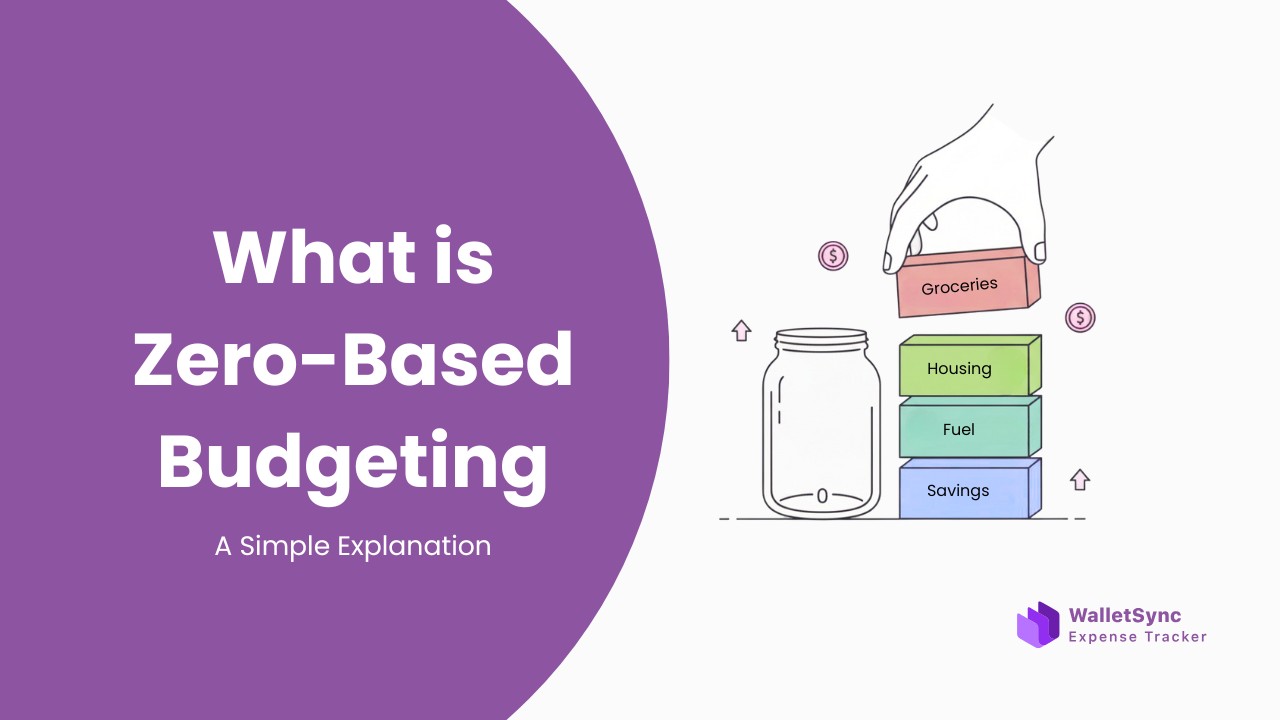

That doesn’t mean you spend everything you earn. Instead, it means that every dollar gets assigned a job, whether it’s for rent, groceries, savings, debt payoff, or even fun money. Nothing is left floating around unaccounted for.

Think of it like giving your money a roadmap. Instead of saying, “I’ll just spend and see what’s left,” you tell every dollar exactly where to go.

Simple formula:

Income – Allocations = Zero

At its core, ZBB asks a simple question for every expense:

“Do we truly need this, and what value does it provide?”

The Two Core Principles of Zero-Based Budgeting

Zero-Based Budgeting is built on two key principles that distinguish it from other budgeting methods:

1. Starting from Zero

At the start of each budget cycle, all expenses are automatically set to zero. No money is assumed to be spent unless a need is proven. This challenges existing spending patterns and ensures every expense is intentional.

2. Justification Is Everything

Every expense, from housing costs and fuel bills to groceries and utilities, must demonstrate its necessity, purpose, and value. This principle fosters accountability and ensures resources are allocated efficiently.

These principles make ZBB a strategic tool, not just a way to cut costs. It’s about intentional resource allocation and making every dollar contribute to your most important goals.

How Does Zero-Based Budgeting Work?

Setting up a zero-based budget is easier than it sounds. By carefully planning where every dollar goes, you gain complete control over your money and avoid surprises at the end of the month.

Here’s how you can set up a zero-based budget in four simple steps:

Step 1: Write down your total income

Example: Let’s say you earn $6,000 a month.

Step 2: List your expenses

Include both fixed costs (like rent or car payments) and variable costs (like groceries, dining out, and entertainment).

Step 3: Assign every dollar a purpose

- Allocate each dollar to a category: bills, savings, debt payments, or fun money.

- Continue until there are no “leftover” dollars.

Step 4: Adjust until income minus allocations = 0

- Check that all your income has been assigned.

- If you still have unallocated funds (e.g., $500), decide where they go: extra savings, debt repayment, or a sinking fund.

Zero-Based Budgeting Example ($6,000/month)

| Category | Amount |

|---|---|

| Rent/Mortgage | $2,000 |

| Groceries | $700 |

| Utilities | $300 |

| Car Payment & Insurance | $600 |

| Savings | $1,000 |

| Debt Repayment | $800 |

| Entertainment & Dining Out | $400 |

| Miscellaneous & Personal Expenses | $200 |

| Total | $6,000 |

Why Do People Use Zero-Based Budgeting?

Zero-based budgeting has gained popularity for a few good reasons:

- Intentional spending: You decide beforehand where your money goes, not after it disappears.

- Helps eliminate waste: You see exactly where your money flows, making it easier to cut unnecessary expenses.

- Promotes saving and debt reduction: Because you’re actively assigning dollars to goals.

- Works for both individuals and organizations: Families use it to manage household money, while companies use it to justify every business expense.

Who is Zero-Based Budgeting For?

ZBB isn’t just for “numbers people.” It can work for:

- Individuals and families who want to stop wondering where their money went.

- Students or first-time budgeters who need structure.

- Businesses and nonprofits that need to justify every expense.

Basically, if you want more control over your money, this method can help.

If you’d like to explore zero-based budgeting further and understand its pros and cons, check out our guide on the advantages and disadvantages of zero-based budgeting.

Conclusion

Zero-based budgeting is a methodical and disciplined approach where every expense must be justified from a blank slate. By focusing on necessity and value, ZBB encourages smarter, more intentional financial decisions that directly align with your priorities.

Try this: Take 5 minutes to map out your next paycheck using zero-based budgeting. You might be surprised at how empowering it feels to give every dollar a purpose.